TL;DR — trading software development in one paragraph

Trading software development is the engineering of platforms that place, route, match and settle trades — retail apps, brokerage systems, algo engines or full exchanges. The hard parts are the same everywhere: real-time market data, an order matching or routing core, risk controls, and financial-grade compliance. In 2026 a single-asset MVP runs about USD 25,000–60,000, a retail brokerage platform USD 60,000–150,000, and a multi-asset or exchange-grade system USD 200,000–500,000 or more. Success is measured in latency, reliability and regulatory correctness, not feature count.

What is trading software development?

Trading software development is the process of building the applications that let people or algorithms place, route, match and settle trades in financial markets — from a retail brokerage app to an institutional order management system or a full exchange with its own matching engine. It combines low-latency backend engineering, real-time market-data handling, a responsive charting front end, and financial-grade security and compliance. What sets it apart from ordinary app development is the standard it is held to: latency, reliability and correctness under load, because a few milliseconds of delay or a single mishandled order can translate directly into financial loss.

Because of that bar, trading platforms are almost always custom-built by a specialist team rather than assembled from generic templates. Most companies that take this on partner with a fintech software development company that already understands market-data feeds, the FIX protocol, exchange connectivity and the regulatory perimeter — the parts that are unforgiving and expensive to learn on the job. Treat the trading engine, the data pipeline and the compliance layer as the heart of the product from day one; the UI is the easy part, and building it first is a common and costly mistake.

What types of trading software can you build?

There is no single “trading platform” — the term covers several distinct products with very different engineering and regulatory profiles. Deciding which one you are building is the first and most important scoping decision, because it drives your latency targets, your data needs and which regulators you answer to. These are the main categories teams commission in 2026.

- Retail brokerage & trading apps. Consumer-facing web and mobile apps for buying and selling stocks, ETFs or crypto, with charts, order tickets and portfolios. The focus is onboarding, usability and connecting to a broker or liquidity provider.

- Institutional OMS / EMS. Order and execution management systems for desks and funds that route large orders across venues, with advanced order types, smart routing and audit trails.

- Exchanges & matching engines. Full venues that host their own order book and match trades in-house — the most demanding build, dominated by latency, throughput and market-integrity requirements.

- Algorithmic & quant trading systems. Engines that run automated strategies, with backtesting, signal processing and pre-trade risk controls; these fall squarely under algorithmic-trading regulation.

- Portfolio & asset management (PMS). Systems for tracking positions, performance, P&L and reporting across accounts, often without direct execution.

- Crypto trading platforms. Spot or derivatives venues and wallets for digital assets; our guide to crypto exchange development cost covers that variant in depth.

Many products blend categories — a retail app may embed a lightweight matching engine, or a PMS may add execution — but naming the primary type keeps scope and compliance honest. Custom trading software development almost always starts here, because the wrong category assumption is the most expensive mistake to unwind later.

What are the core features of a trading platform?

Every serious trading platform shares a common backbone of features, regardless of asset class: real-time data, order handling, risk control and compliance reporting. The visible UI is only the surface; most of the engineering effort and cost lives in the data and execution layers underneath. The checklist below is the practical baseline for a 2026 build — use it to scope your MVP and to sanity-check any vendor proposal.

- Real-time market data & charting. Streaming quotes, order-book depth and candlestick charts with sub-second updates — typically the most resource-intensive part of the system.

- Order management & execution. Multiple order types (market, limit, stop, stop-limit), order lifecycle tracking, and routing to a matching engine, broker or liquidity venue.

- Portfolio, positions & P&L. Live balances, holdings, realised and unrealised profit-and-loss, and transaction history.

- Risk management & pre-trade controls. Position limits, price collars, kill-switches and margin checks — a hard regulatory requirement, not an optional add-on.

- Onboarding, KYC & AML. Identity verification, sanctions screening and account management; see our KYC and AML software development guide for what that layer involves.

- Funding, payments & settlement. Deposits, withdrawals and clearing, which usually means integrating a payment and banking layer — our payment gateway integration guide maps the options and PCI scope.

- Reporting, audit trail & compliance. Immutable logs of every order and event, regulatory reports, and best-execution records.

- Alerts, watchlists & APIs. Price alerts, an economic calendar, and public or partner APIs for market data and programmatic trading.

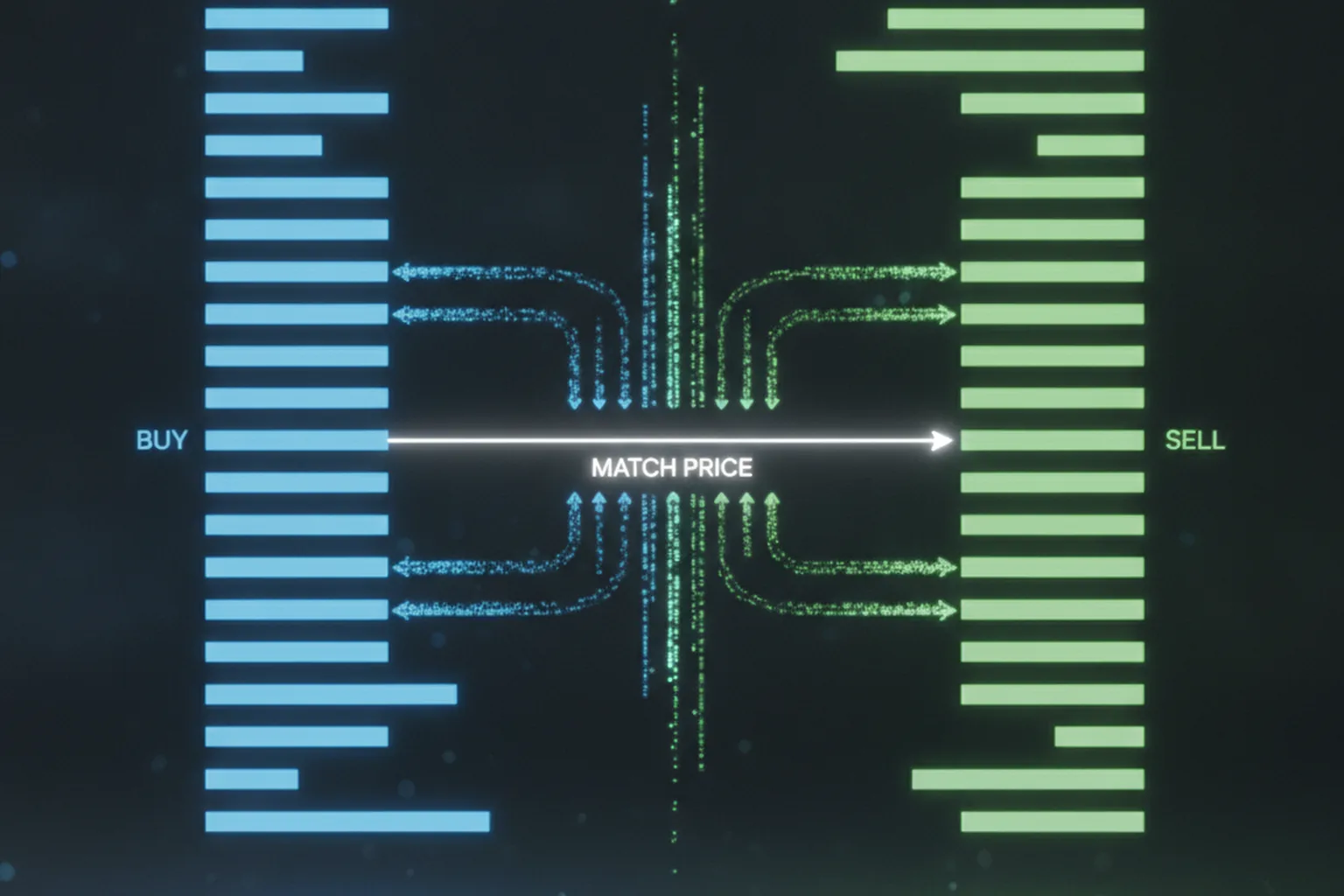

How does an order matching engine work?

An order matching engine is the core of any exchange or trading venue: it keeps an order book of resting buy and sell orders and pairs them using deterministic rules, most commonly price-time priority. Under price-time priority the best-priced order is filled first, and when two orders share the same price, the one that arrived earliest wins. When an incoming buy order crosses a resting sell order (or vice versa), the engine executes the trade, updates the book, and publishes the result to every subscriber — ideally within microseconds.

Two engineering properties make or break a matching engine. The first is determinism: given the same sequence of orders, it must always produce the same result, because fairness and auditability depend on predictable ordering. The second is market-data fan-out: once a trade executes, the venue has to broadcast order-book and trade updates to thousands of subscribers at once, which is why teams build robust bidirectional WebSocket or multicast pipelines, minimise payload size, and often reach for in-memory data structures and low-level languages. If you are routing to an existing venue rather than hosting your own book, you skip the matching engine but inherit the same market-data and latency challenges on the client side.

What tech stack do you need for trading software?

The right stack for trading software is chosen around latency, throughput and reliability first, and developer convenience second — the opposite priority order from most consumer apps. That said, you do not need exotic technology everywhere; the low-latency discipline concentrates in the execution and data path, while the rest of the system can use mainstream tools. A typical 2026 architecture looks like this:

- Execution & matching core: a low-latency language such as C++, Rust, Java or Go, often with in-memory order books and lock-free data structures.

- Market data & messaging: the FIX protocol for venue connectivity, plus streaming infrastructure (WebSocket, Kafka or multicast) and a time-series database for tick data.

- Front end: React or a similar framework with TypeScript and a dedicated charting library built for high-frequency updates.

- Infrastructure: cloud for most services, with colocation or bare metal near the exchange when microseconds matter; autoscaling for market-data spikes.

- Security & data: encryption in transit and at rest, hardened authentication, secrets management, and full audit logging.

The stack is a means to an end: predictable performance and an order path you can prove correct. If your team is weighing broader architecture questions before committing, our custom software development team can help match the design to your latency budget and asset classes rather than defaulting to a one-size-fits-all template.

How much does trading software development cost in 2026?

In 2026, a single-asset MVP or validation build typically costs about USD 25,000–60,000, a retail brokerage or equity trading platform runs roughly USD 60,000–150,000, and a multi-asset or advanced platform with real-time data, advanced charting and payments commonly reaches USD 200,000–500,000 or more. A custom algorithmic or quant trading engine usually lands between USD 80,000 and 300,000. Read these as planning ranges rather than quotes — the table below shows how build type maps to cost and time.

| Build type | Typical 2026 cost (USD) | Typical time to launch |

|---|---|---|

| Single-asset MVP (validation) | $25k–$60k | 3–4 months |

| Retail brokerage / equity platform | $60k–$150k | 4–7 months |

| Algorithmic / quant trading engine | $80k–$300k | 6–12 months |

| Multi-asset / exchange-grade platform | $200k–$500k+ | 8–16 months |

| Run, market data & compliance (per year) | ~15–25% of build | Continuous |

Four factors move the number most: the number of asset classes, your latency requirements, how many market-data and broker integrations you need, and your regulatory scope. Recurring costs are easy to underestimate — market-data feeds, exchange connectivity and compliance tooling can rival engineering as an ongoing line item. To turn these ranges into a defensible budget for your own product, work through our software project estimation guide, which breaks estimating down stage by stage instead of relying on one lump-sum guess.

Trading software compliance: SEC, FINRA and MiFID II

Compliance is not a phase you add at the end of trading software development — it shapes the architecture, because supervision, audit trails and pre-trade risk controls have to be built into the order path itself. In the US, the SEC, FINRA and CFTC set the rules; in the EU, MiFID II and its RTS 6 standard, supervised by ESMA, govern algorithmic trading. Regulators are explicitly technology-neutral, meaning the same obligations for recordkeeping and risk management apply whether a human or an algorithm places the order. The table summarises the frameworks most builds have to design around.

| Framework | Jurisdiction | What it governs |

|---|---|---|

| SEC (Reg NMS, Reg ATS, Rule 15c3-5) | US equities & venues | Fair access, alternative trading systems, market-access pre-trade risk controls |

| FINRA (Rule 3110, Notice 15-09) | US member firms | Supervision, algorithmic-strategy testing, audit trails |

| CFTC | US futures & derivatives | Registration, audit trails, pre-trade risk limits |

| MiFID II / RTS 6 (ESMA) | EU / EEA | Algorithmic-trading controls, stress testing, pre-trade limits, records |

| EU AI Act | EU / EEA | AI systems used within algorithmic-trading workflows |

In February 2026, ESMA published a supervisory briefing on algorithmic trading under MiFID II, pushing for closer alignment across the EU on stress-testing, outsourcing, pre-trade controls and the use of AI in trading workflows — a signal that scrutiny of automated trading is tightening, not loosening. The practical takeaway for a build: design the audit trail, kill-switch and pre-trade risk checks in from the start, keep testing environments separate from production, and document everything. Retrofitting these later is far more expensive than building them in.

What is the trading software development process?

Trading software development follows a disciplined sequence in which regulatory scoping and architecture come before any user-facing feature, because the hardest constraints — latency, correctness and compliance — are cheapest to satisfy when designed in from the start. The process below is the path most successful 2026 builds follow.

- Discovery & regulatory scoping. Fix the platform type, asset classes, target markets and the regulators that apply. This decides everything downstream, so it comes first.

- Architecture & data design. Design the execution path, market-data pipeline and risk layer to your latency budget, and choose venues, feeds and the FIX connectivity you need.

- Build the core. Implement the matching or order-routing engine, order management and pre-trade risk controls — the parts that must be correct under load — before the UI.

- UX, charting & integrations. Add the front end, real-time charts, and integrations for KYC/AML, payments and settlement.

- Testing & certification. Backtest strategies, run load and failover tests, and validate compliance controls in an environment kept fully separate from production, per FINRA guidance.

- Launch & monitoring. Go live with real-time monitoring, alerting and an incident playbook; in trading, observability is a launch requirement, not a follow-up.

How to choose a trading software development company

Choose a trading software development company on proven fintech and market-infrastructure experience, not on the day rate alone — a general agency that has never handled market data, the FIX protocol or a regulator will learn on your budget and your risk. You want a team that treats latency, correctness and compliance as first-class engineering concerns and can show it. When comparing trading software development companies, weigh these signals:

- Real trading or market-infrastructure projects. Ask specifically for brokerage, exchange or algo-trading work they have shipped, and what latency and volume it handled.

- Regulatory fluency. The right partner speaks SEC, FINRA and MiFID II comfortably and designs audit trails and risk controls in from day one.

- Low-latency engineering depth. Look for senior engineers who understand order books, matching, market-data fan-out and the FIX protocol — not just app developers.

- Security & data governance. Financial-grade encryption, secrets management, and clear data-handling practices are non-negotiable.

- Transparent pricing and ownership. Clear stage-by-stage estimates, regular demos, and written confirmation that you own the code and IP.

For a fuller vendor-evaluation framework you can apply to any build, see our guide on how to choose a software development company. The trading-specific twist is simple: prioritise market-infrastructure experience and regulatory fluency over the lowest hourly rate, every time.

FAQ

What is trading software development?

Trading software development is the process of building the applications that let people or algorithms place, route, match and settle trades in financial markets — from a retail brokerage app to an institutional order management system or a full exchange with its own matching engine. It combines low-latency backend engineering, real-time market data handling, a responsive charting front end, and strict financial-grade security and regulatory compliance. Unlike ordinary apps, trading software is judged on latency, reliability and correctness under load, because a few milliseconds or a mishandled order can mean real financial loss.

How much does trading software development cost in 2026?

In 2026, a single-asset MVP or validation build typically costs about USD 25,000 to 60,000, a retail brokerage or equity trading platform runs roughly USD 60,000 to 150,000, and a multi-asset or advanced platform with real-time data, advanced charting and payments commonly reaches USD 200,000 to 500,000 or more. A custom algorithmic or quant trading engine usually falls between USD 80,000 and 300,000. Budget a further 15 to 25 percent of the build cost per year for running, market-data fees and compliance. The biggest cost drivers are asset classes, latency requirements, the number of market-data and broker integrations, and regulatory scope.

How does an order matching engine work?

An order matching engine is the core of an exchange or trading venue: it maintains an order book of buy and sell orders and pairs them using rules such as price-time priority, where the best price is filled first and, at equal prices, the earliest order wins. When a buy and a sell order cross, the engine executes the trade, updates the order book, and broadcasts the result to all subscribers in real time. Matching engines must be extremely fast and deterministic, because throughput and predictable ordering are what make a market fair and usable.

What regulations apply to trading software?

In the US, trading software is governed by the SEC (Reg NMS, Reg ATS and the Market Access Rule 15c3-5), FINRA (supervision under Rule 3110 and algorithmic-testing guidance in Notice 15-09), and the CFTC for futures and derivatives. In the EU, MiFID II and its RTS 6 technical standard set requirements for algorithmic trading controls, stress testing, pre-trade risk limits and record-keeping, supervised by ESMA. Regulators treat their rules as technology-neutral, so obligations for supervision, audit trails and risk controls apply whether trades are manual or algorithmic; AI-driven trading may additionally fall under the EU AI Act.

How long does it take to build a trading platform?

A focused single-asset trading MVP usually takes about three to four months, a retail brokerage or equity platform four to seven months, and a multi-asset or exchange-grade system eight to sixteen months or more. Timelines stretch with the number of asset classes, latency targets, market-data and broker integrations, and regulatory approvals, which can run in parallel but add lead time. Because market data, compliance and risk controls are unavoidable even in a first version, trading software rarely ships as fast as a general consumer app of similar size.

Last updated 15 July 2026. Cost and timeline figures are 2026 planning ranges drawn from typical US and EU trading-software engagements and are offered as general guidance, not quotes. Regulatory references (SEC, FINRA, CFTC, MiFID II / RTS 6, ESMA, EU AI Act) are for orientation and are not legal advice — confirm your obligations with qualified counsel. Your real budget, schedule and compliance scope depend on asset classes, latency, integrations and jurisdiction.