Card scope creep

PCI DSS audit scope quietly grows with every new microservice. We tokenize early and isolate cardholder data to keep the audit boundary small.

GDPR PCI DSS AI-native

YuSMP Group builds production fintech software for payments, lending, wallets, neobanks and capital-markets desks across the US and EU. Eighty senior engineers ship inside PCI DSS software development scope, partner with QSAs on assessments, and deliver KYC/AML, open banking and real-time payment flows that satisfy regulator-grade scrutiny. xRouten payment routing improved auth rates by 4.1 points and cut latency 38%.

We deliver custom fintech engineering for four buyer profiles: payment processors and PSPs moving card, ACH, SEPA and FedNow volume; consumer and SMB lenders running KYC/AML, underwriting and servicing; wallet, BNPL and neobank teams building on banking-as-a-service rails; and capital-markets desks integrating market data, execution and post-trade workflows. Our delivery teams operate inside PCI DSS scope, coordinate assessments with partner QSAs, and design to PSD2, open banking, FedNow, SEPA and US state money-transmitter expectations. GDPR alignment, SOC 2 Type II progress and ISO 27001 readiness sit underneath every engagement. Explore how we deliver this through our Custom Software Development service.

Challenges

PCI DSS audit scope quietly grows with every new microservice. We tokenize early and isolate cardholder data to keep the audit boundary small.

Strong customer authentication kills conversion when applied bluntly. We tune risk-based exemptions and 3DS2 flows for measurable uplift.

Mainframe and aging core banking systems block product velocity. We wrap them with event-driven facades and progressive strangler patterns.

Rule-only monitoring drowns analysts in false positives. We add ML scoring and feedback loops to lift true-positive rate without breaking auditability.

ICT risk register, third-party concentration and resilience testing are now non-negotiable. We engineer them in, not bolt them on.

Multi-jurisdiction deployments need careful data residency and SCC handling. EU data residency by default, US options on request, with clear lawful basis.

Solutions

Acquiring, issuing and orchestration with token vaults, 3DS2, refunds and reconciliation across US & EU schemes.

Origination, decisioning, servicing and collections with explainable scoring models and regulatory reporting.

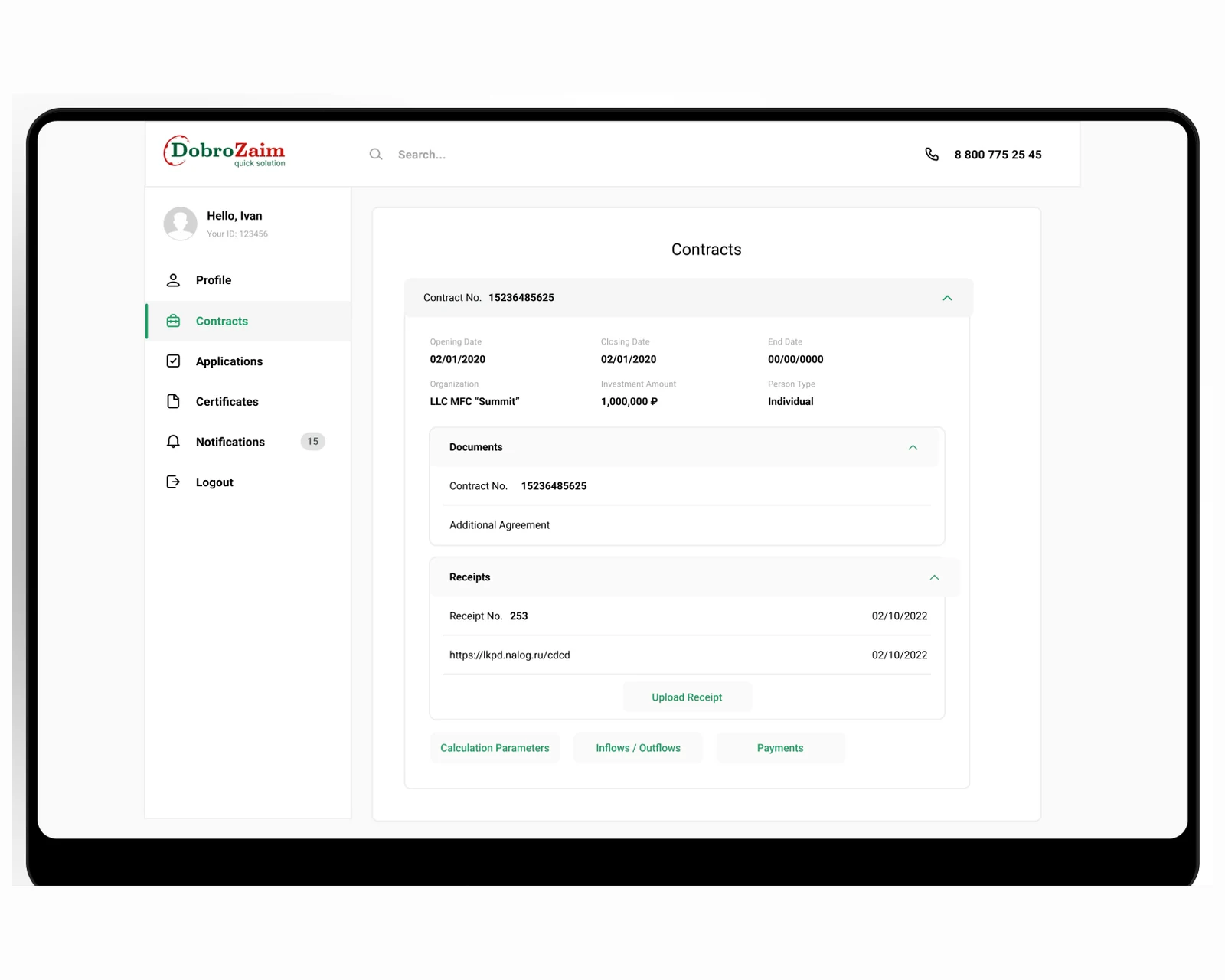

Core ledger, accounts, cards, FX and onboarding stacks for licensed EMIs and challenger banks.

Order management, market data, execution and post-trade for retail and pro investors under MiFID II.

Identity verification, sanctions and PEP screening, transaction monitoring, SAR/STR case management.

Banking-as-a-Service APIs, partner onboarding, white-label wallets and revenue-share reporting.

Stack

Java, Kotlin, Go, Node.js, TypeScript, Python, PostgreSQL, Kafka, Redis, Temporal, Kubernetes, Terraform, AWS, GCP, Vault, OpenSearch.

Compliance

GDPR-aligned · ISO 27001 ready · SOC 2 Type II in progress · HIPAA-capable · CCPA-acknowledged

Shared: PCI DSS v4.0 — tokenization, scope reduction, audit-ready logging.

On this page each regime is framed as a fintech delivery challenge. For the step-by-step control implementation and audit path, see our dedicated PCI DSS software development, GDPR compliance consulting and SOC 2 readiness services.

Integrations

Fintech products live or die on their connections. Our engineers build against the rails, schemes and data providers that US and EU financial products depend on — cleanly abstracted so a provider can be swapped without re-architecting.

Visa, Mastercard, American Express and Discover flows with EMV 3DS2, network tokenization and acquirer/processor connectivity for both issuing and acquiring.

ACH under NACHA, FedNow and TCH RTP in the US; SEPA Credit Transfer, SEPA Instant and SEPA Direct Debit plus SWIFT and Fedwire for cross-border payments and wires.

PSD2 account-information and payment-initiation flows through licensed AISP/PISP providers and aggregators such as Plaid, MX and Mastercard Open Banking for account verification and pay-by-bank.

Document and biometric identity verification, sanctions and PEP screening against OFAC, EU consolidated and UN lists, and transaction-monitoring feeds wired into SAR/STR workflows.

Core-banking and card-issuing processors, Banking-as-a-Service partner rails and a double-entry ledger of record for accounts, balances and reconciliation.

Market-data feeds, order-management and execution over FIX, plus custody, settlement and post-trade reconciliation for trading and brokerage desks under MiFID II.

Need a specific integration scoped? Our custom software development and cloud & DevOps teams own the build and the runtime.

Process

Every engagement is compliance-enforced from the first architecture decision, not audited into shape at the end.

We map the regimes in scope — PSD2, DORA and MiCA in the EU, or GLBA, SEC, FFIEC and BSA/AML under FinCEN in the US — and define PCI DSS boundaries before a line of code is written.

Token vaults and cardholder-data isolation keep the PCI audit boundary small; data residency is EU-default with US options, and lawful basis is decided up front.

Engineers ship inside PCI scope with KYC/AML controls, PSD2 SCA and 3DS2 flows, sanctions screening and threat models built into each increment.

We coordinate assessments with partner QSAs, run DORA-aligned resilience testing and certify integrations against scheme and rail requirements before launch.

Each release ships with traceable change records, SBOMs and threat-model deltas, plus incident classification and third-party monitoring to keep resilience evidence audit-ready.

We stay on as a long-term engineering partner — tracking regulatory change, tuning AML rules and evolving the platform as your licences and markets expand.

Cases

A high-throughput loan decision engine on Laravel — automated scoring, credit-bureau integration, and 10x faster decisions for US & EU lenders.

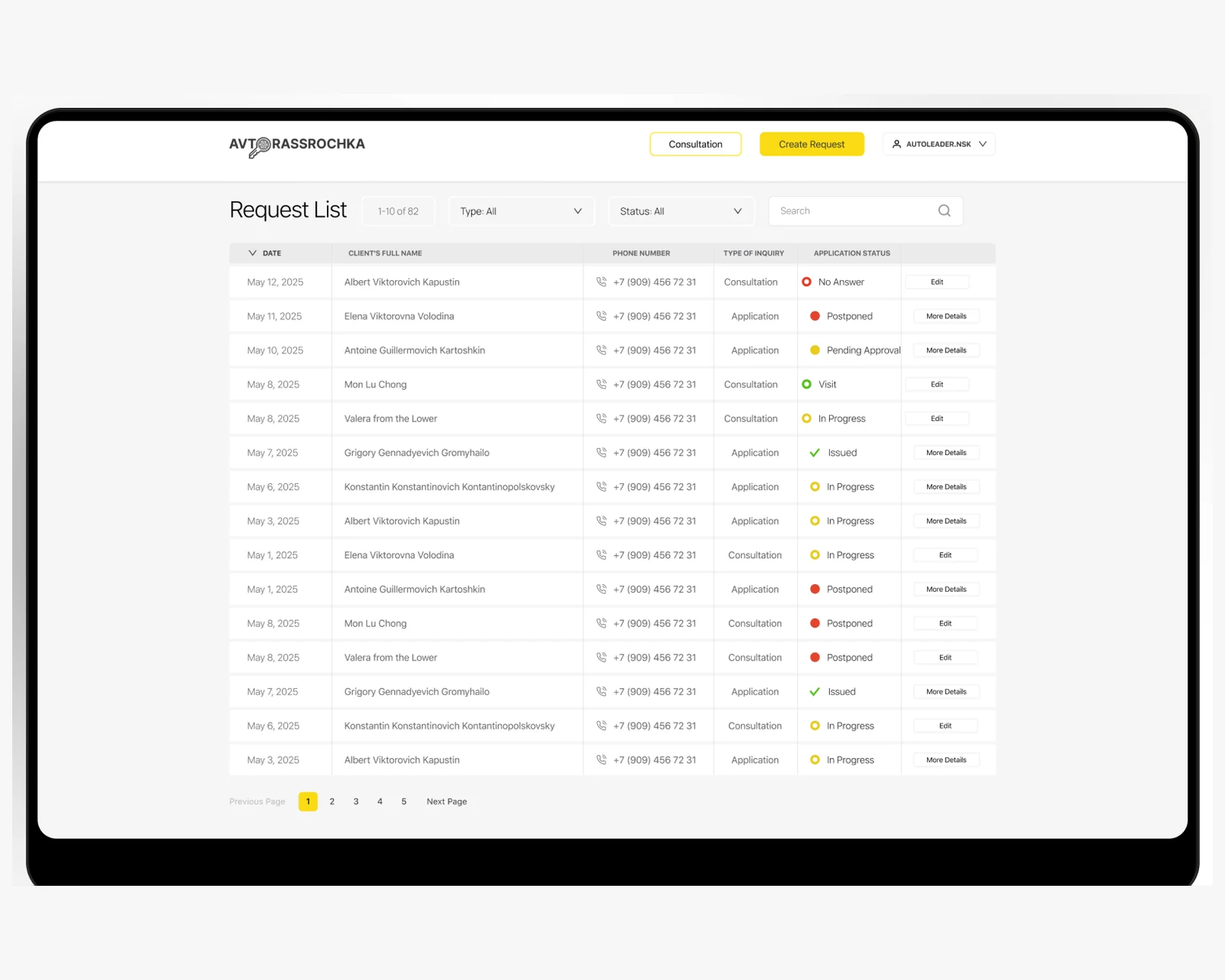

Dealer-facing web platform funneling every auto-financing enquiry into a single tracked queue with Bitrix24 CRM sync.

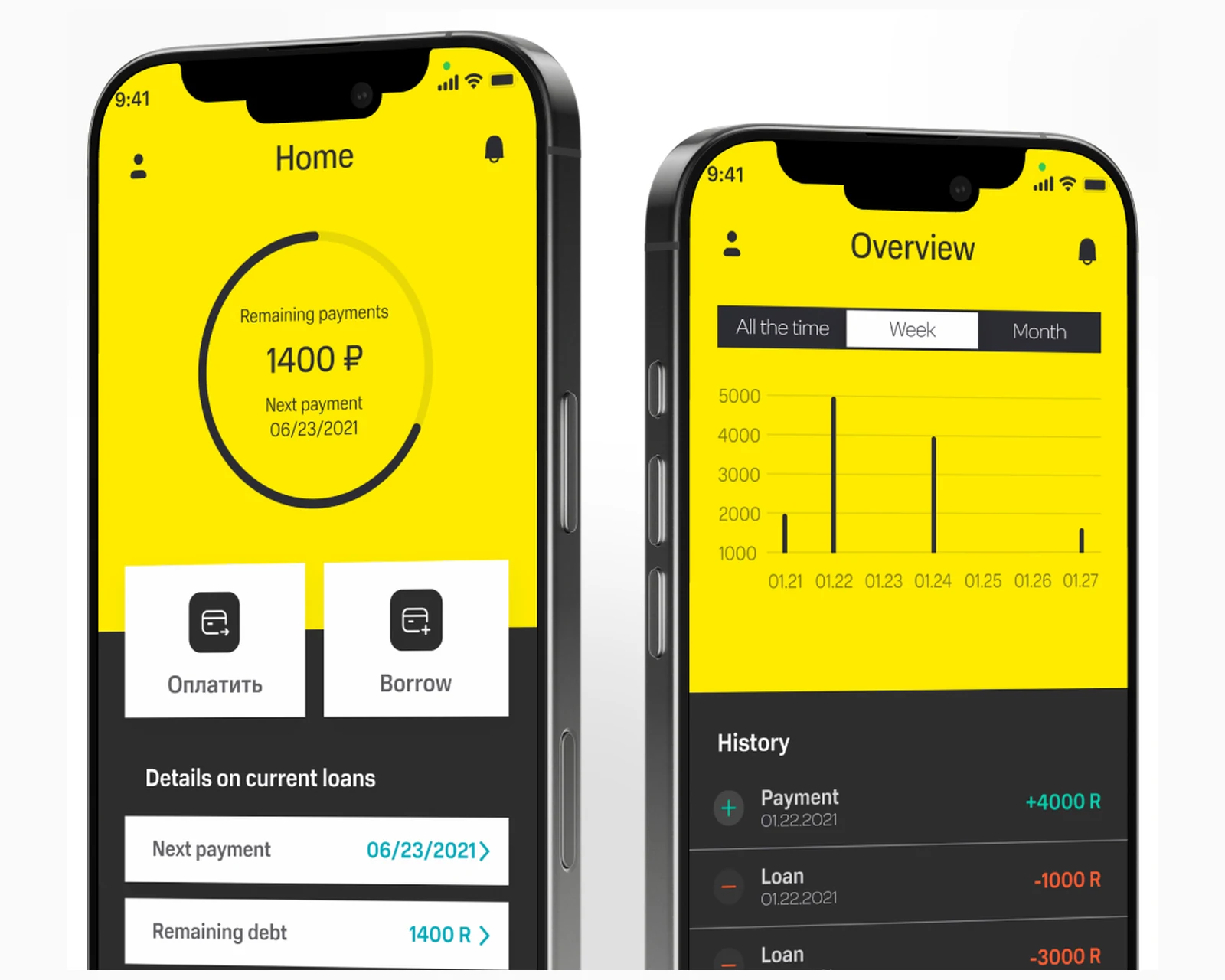

Laravel + React microloans platform — borrower dashboard with e-signature, underwriter workstation, collections, accounting, admin.

Why YuSMP

Senior engineers fluent in PSD2, DORA, MiCA (EU) and GLBA, SEC, FFIEC (US) — not learning on your audit.

EU data residency by default (Frankfurt, Dublin, Stockholm) · US options on request (us-east-1, us-west-2). SCCs only when truly needed.

Every release ships with traceable change records, SBOMs and threat-model deltas.

Aggregating live prices across multiple exchanges while keeping latency under 500 ms is genuinely hard engineering. YuSMP built the multi-exchange feed, real-time token charts, and listing workflow into a coherent platform. We have not had an outage since launch.

A loan decision engine that takes ten times less time to approve does not happen by accident. YuSMP built the scoring pipeline, integration with credit bureaus, and a back-office that our underwriters actually enjoy using. Approval turnaround went from two days to under four hours.

FAQ

Yes. We design card-handling architectures with tokenization, scope reduction and audit trails aligned with PCI DSS v4.0, and partner with QSAs for formal certification.

We implement PSD2 SCA with risk-based exemptions, 3DS2 flows and account information service connectivity through licensed AISP/PISP providers. For US flows we align with Reg E, NACHA WEB debit authentication and FFIEC multi-factor guidance.

We map ICT risk, set up incident classification, third-party register and resilience testing in line with DORA articles 5-15 from day one of architecture. For US clients we mirror the program against FFIEC IT examination guidance and SEC Reg S-P safeguards.

We implement GLBA Safeguards Rule controls, SEC Rule 10b-5 anti-fraud surveillance for trading, FFIEC-aligned IT exam readiness and BSA/AML programs under FinCEN — including CIP, SAR/CTR filings and OFAC sanctions screening.

Yes. We deliver custody, exchange and tokenization platforms with MiCA-aligned governance, market abuse controls and travel rule integration.

We integrate identity providers, sanctions and PEP screening, transaction monitoring with adjustable rule engines and ML scoring, and SAR/STR workflows.

Response within 1 business day. NDA on request.

In-depth guides on building compliant fintech apps — cost, stack and security.

Share a few details and a senior consultant will reply within one business day.