Discovery & latency audit

Profiling the existing decision path, mapping every synchronous external call and risk rule, and setting the latency budget and GDPR + CCPA data-ownership posture.

Case study · FinTech · Lending

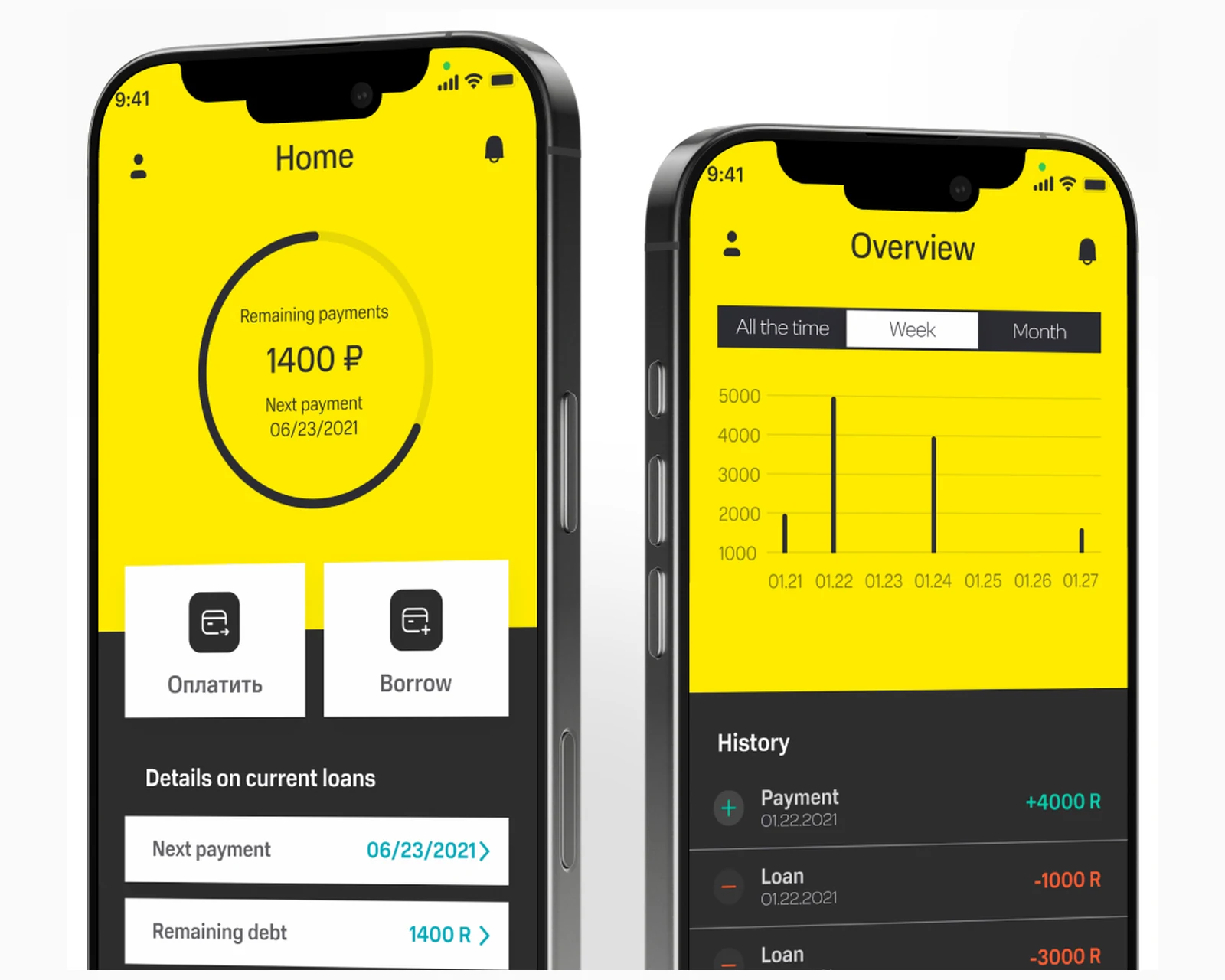

How we rebuilt the decision-making core of an online lending portal as a dedicated, high-throughput scoring service — automated credit scoring, credit-bureau integration, and session-stable origination — that cut the time to a loan decision from roughly 15 minutes to about 1.5, built for lenders across the United States and the European Union under GDPR and CCPA expectations from day one.

The client was a high-volume online lender whose origination portal already worked end to end, but whose decision-making module had become the single point that slowed everything down. For lenders in the United States and the European Union, that latency is not a cosmetic problem — every extra minute an applicant waits for an approve-or-decline answer is a minute in which a competitor's faster offer can win the deal, and applications that hang long enough are simply abandoned. The decision step took on the order of 15 minutes per application, the user session frequently timed out before a result came back, and the slow module dragged on the throughput of the rest of the portal. The brief was to make decisions dramatically faster without weakening the underwriting itself: keep the same rigorous assessment of credit history, employment, property, and work experience, but deliver the answer in a fraction of the time and stop losing applicants mid-flow. We rebuilt the decision core from first principles at YuSMP Group as a dedicated scoring service — automated applicant analysis, credit-bureau integration, and an asynchronous, session-stable origination path — engineered with our custom software development practice for the US and EU markets.

A snapshot of what the Loan Conveyor decision-engine rebuild delivered for the lending portal in its first production cycle.

The architecture decision dominated every other choice in this build. We chose to extract decisioning into a dedicated, asynchronous scoring service rather than keep optimizing the in-portal module, because the latency that pushed applicants to abandon their sessions was structural. The old path ran external lookups and risk rules in sequence on the request thread, holding the user's session open while a slow credit-bureau call or an unbounded scoring step ran to completion. No amount of in-place tuning closes a 10x gap when the work itself is serialized and synchronous. A dedicated service let us own the full latency budget, parallelize the independent inputs, and decouple the applicant's session from the underwriting work entirely.

The trade-off teams underweight is reproducibility under speed. Making decisions faster is easy if you are willing to skip checks; the hard part is keeping the exact same rule set — credit history, employment, property, work experience — running every time so a decision stays deterministic and auditable for lenders answering to US and EU regulators. We kept the underwriting logic intact and bought the speed from architecture: concurrent inputs, strict external timeouts with sane fallbacks, and a bounded scoring path that a slow bureau can never stall. The whole engine is open and maintainable for the long run rather than locked behind a packaged vendor's roadmap.

| Dimension | Dedicated service (this build) | In-portal decision module | Packaged decisioning SaaS |

|---|---|---|---|

| Time to decision | ~1.5 min, bounded | ~15 min, unbounded | Varies; per-call pricing |

| Scoring execution | Parallel, asynchronous | Serialized on request thread | Opaque, vendor-controlled |

| Session stability | Session decoupled from work | Session held open, times out | Depends on integration |

| Bureau integration | Native, timeout-guarded | Blocking, single-threaded | Bundled, less control |

| Rule reproducibility | Deterministic, audit-logged | Same logic, slow | Black-box model |

| Data ownership (GDPR / CCPA) | Full ownership and residency | Owned, but coupled | Vendor-hosted, shared |

| Portal-wide throughput impact | Isolated, no contention | Drags the whole portal | External dependency risk |

Platform references: Laravel documentation, Laravel queues & jobs, Redis documentation.

The origination flow starts at the application form, where an applicant supplies loan amount, monthly income, purpose, and identity details. The Laravel backend takes that submission and, instead of blocking the page while it works, hands the application to an asynchronous scoring pipeline. The independent inputs that drive a decision — credit-bureau history, employment and property assessment, and the lender's internal risk rules — are dispatched to run concurrently rather than one after another, so the slowest single input, not the sum of all of them, sets the floor on how long a decision takes. That one structural change is the largest contributor to the move from a roughly 15-minute wait to about 1.5.

Each external call is wrapped with a strict timeout and a sane fallback, so a slow or unavailable credit bureau degrades gracefully into a manual-review path instead of stalling the queue behind it. The scoring path itself is bounded and deterministic: the same rule set runs every time and writes an audit-ready decision record, which matters for lenders that have to explain an approve-or-decline outcome. The full origination backend was delivered as part of our custom software development practice for US and EU lenders.

The decision quality lives in the external data and how the engine reads it. We integrated the lender's credit-history sources so the engine pulls an applicant's bureau record automatically rather than waiting on a manual lookup, then layered the lender's own assessment of employment status, property, and work experience on top. Each of those inputs is normalized into a common shape the scoring rules can reason about, so adding a new signal later is a configuration change against the analysis layer rather than a rewrite. Because the bureau call is the most variable dependency in the whole flow, it gets the strictest timeout and the clearest fallback in the system.

Applicant analysis runs the same way for every application, which is what keeps the faster decisions trustworthy. The engine does not shortcut checks to gain speed; it gains speed by running the checks concurrently and caching what is safe to cache. The result is a single, reproducible score backed by a record of exactly which inputs produced it — the foundation a lender needs to satisfy GDPR data-handling obligations for applicants in the European Union and CCPA / CPRA obligations for applicants in California and the broader United States. The data and integration layer is engineered on our cloud & DevOps foundation so bureau connectors, scoring workers, and the API scale together.

Session stability is the backbone that turned long waits into completed applications. We moved scoring off the request thread into background jobs and let the front end receive the result when it lands, so the applicant sees clear progress instead of a frozen, timing-out page. Long-running external lookups are isolated so one slow dependency can never exhaust the web tier, and partial application state is persisted so a dropped connection resumes rather than restarts. Removing the session timeout that used to lose applicants mid-decision is, alongside raw speed, why fewer borrowers abandoned the flow.

Because the lender owns the deployment, data ownership and residency are design choices rather than vendor defaults. Applicant data can be pinned to US or EU infrastructure for future data-residency commitments, role-based access separates underwriter, manager, and admin views, and every decision is logged with the inputs that produced it. The system aligns with GDPR obligations for applicants in the European Union and CCPA / CPRA obligations in the United States — making a future readiness review a documentation exercise rather than an architectural retrofit.

Compliance posture: GDPR-aligned · ISO 27001 ready · SOC 2 Type II in progress · HIPAA-capable · CCPA-acknowledged.

A five-phase build, run on a Scrum cadence with weekly client reviews, that took the decision engine from a 15-minute bottleneck to a sub-two-minute service live in production.

Profiling the existing decision path, mapping every synchronous external call and risk rule, and setting the latency budget and GDPR + CCPA data-ownership posture.

Dedicated scoring service, asynchronous job queue, parallel bureau and employment/property inputs, and the bounded, deterministic scoring contract.

Laravel decision engine, credit-bureau integration, applicant analysis layer, timeout-guarded fallbacks, and audit-ready decision logging.

Concurrency tuning, session-stability QA, fallback testing against slow bureau responses, and end-to-end timing validation under production-like volume.

Phased cutover into the live portal, decision telemetry, and monitoring across US and EU deployments with weekly review checkpoints.

Beyond the scoring rules themselves, the platform's resilience comes from the asynchronous decision queue that sits between the applicant's session and the underwriting work. Every application becomes a job with its own bounded lifecycle, and the queue backs the work with idempotent processing so a retried decision never produces a duplicate or a contradictory record. When a credit bureau is slow or briefly unavailable, the timeout fires and the application is routed to a manual-review fallback rather than left to hang — the queue keeps moving and no single dependency can cascade into a portal-wide slowdown. That isolation is what protects the rest of the lending portal, which was the original symptom the client came to us with: a slow decision module that dragged on everything around it. The queue is structured so a new scoring input, an additional bureau connector, or a future explainable-model overlay can be added as a configuration change rather than a rewrite, and so volume can scale across US and EU sites by adding workers rather than re-architecting. It is the layer that turns a faster decision into a dependable one, and it is where the platform earns its keep for lending operations that have to commit to a service-level answer time for every applicant.

The decision engine shipped as a single English-language build serving lending operations across the United States and the European Union, without a separate codebase per region. It serves lenders and applicants in California, New York, Texas, Florida, and Washington in the US, and in the Netherlands, Germany, France, Ireland, and Sweden in the EU. Because the lender owns its own deployment, data-handling practices are aligned with GDPR for applicants in the EU and with the US state-privacy patchwork — CCPA / CPRA (California), VCDPA (Virginia), CPA (Colorado), CTDPA (Connecticut), UCPA (Utah), TDPSA (Texas), and Oregon CPA. Role-based access separates underwriter, manager, and admin views, every decision is logged with the inputs that produced it, and applicant data can be pinned to US or EU infrastructure for future data-residency commitments — so regional compliance reduces to honest disclosure and access discipline rather than per-jurisdiction rework.

The engine is built to roll out across EU and US lending operations in parallel, with each deployment's scoring workers and bureau connectors provisioned identically and bound to the local data sources in each region. The same deterministic rule set runs everywhere, so a multi-market lender gets one consistent, explainable decision path across geographies. The engineering team behind the build runs a CET workday with East-Coast US overlap (9 AM–1 PM ET) for stand-ups, integration choreography, and incident response — the window that lets a US lending team and an EU engineering team share four hours of live overlap every day. Data-handling references are documented directly against GDPR obligations and California CCPA obligations.

The active custom software development roadmap for the Loan Conveyor engine includes an explainable scoring overlay that surfaces the reasons behind each decision, additional credit-bureau connectors for multi-market coverage, and a model-monitoring harness that tracks decision drift over time. A configurable rules studio is planned so risk teams can adjust underwriting policy without a code release, and deeper anti-fraud signals are scheduled to join the parallel scoring inputs. Infrastructure plans include further queue-worker automation, a continuous decision-integrity harness that reconciles every logged outcome against its inputs, and regional deployment scaffolded into the cloud & DevOps roadmap for US and EU lenders.

If you are planning a loan origination platform, a credit decision engine, or any fintech backend where decision latency is costing you completed applications for audiences in the US and EU, we have shipped this stack end-to-end and can compress the build timeline meaningfully. The project overview is available at yusmpgroup.ru (web origination backend), and the engineering team behind it sits inside YuSMP Group. We work fixed-price for well-scoped MVPs and on dedicated development teams for ongoing delivery, with a CET workday and a guaranteed East-Coast US overlap (9 AM–1 PM ET) window for stand-ups, demos, and incident response.

A loan decision engine MVP covering automated scoring, one credit-bureau integration, applicant data analysis, and a rules-based underwriting flow typically costs $80k–$200k. Adding multiple bureau connections, an explainable scoring model, employment and property verification, and session-stable origination at high volume brings a full origination backend to $240k–$550k. The dominant cost drivers are the external data integrations, the latency budget for sub-two-minute decisions, and the audit-ready decision logging that lenders in the US and EU require.

When a decision module is the bottleneck slowing the whole origination portal, incremental tuning rarely closes a 10x gap. The wait that pushes applicants to abandon a session usually comes from synchronous external calls, an unbounded scoring path, and a request lifecycle that holds the session open while it works. Rebuilding the module as a dedicated, asynchronous scoring service lets you control the latency budget end to end, parallelize bureau lookups, and keep the user session stable — improvements that a packaged tweak cannot reach.

Speed comes from architecture, not from skipping checks. We parallelize the independent inputs — credit-bureau history, employment and property assessment, and internal risk rules — so they run concurrently rather than in sequence, then converge on a single deterministic decision. Each input is cached where it is safe to do so, external calls have strict timeouts with sane fallbacks, and the scoring path is bounded so a slow bureau never stalls the queue. The same rule set runs every time, so faster decisions stay reproducible and auditable.

The session must never hang on the decision. We moved scoring off the request thread into a background job and let the front end poll or receive a push when the result lands, so the applicant sees progress instead of a frozen page. Long-running external lookups are isolated so one slow dependency cannot exhaust the web tier, and partial state is persisted so a dropped connection resumes rather than restarts. That session stability is what turned long waits into completed applications instead of abandoned ones.

A focused loan decision engine with automated scoring, one bureau integration, applicant analysis, and rules-based underwriting typically takes 12–20 weeks. Adding additional bureau connections, an explainable model, employment and property verification, and a hardened asynchronous queue for high volume adds 6–10 weeks. For this build the full backend was delivered in roughly four months, deployed into the lender's existing production portal with no downtime through a phased cutover.

Related cases

A fast online lending portal with streamlined application intake and origination flow for borrowers across US & EU.

View case →

A digital-asset platform with wallet integration, exchange flows, and a hardened financial backend across US & EU.

View case →

A crypto product build covering custody, transactions, and a real-time trading backend for US & EU users.

View case →

Custom platforms engineered to your business model, scaling cleanly from MVP to millions of users.

Explore custom software development →

High-throughput web platforms and APIs engineered for reliability under real production load.

Explore web application development →

Containerized infrastructure, CI/CD pipelines, and Terraform-managed deployments across US & EU regions.

Explore cloud & DevOps →Share a few details and a senior consultant will reply within one business day.